Recommended Blog Posts

- LOA and PAL: The Dual Keys to Your 2026 Canada Study Permit

- Study Agriculture and Crop Research in Canada: Admission Process, Eligibility, and Scholarships for International Students

- What Is Bill C-12 and How It Impacts Your Canada Study Visa Application

- How to Write a Perfect SOP for Canada Study Visa Approval in 2026

- How to Convert a Visitor Visa to a Study Permit Without Leaving Canada (2026 Guide)

Study Permit Proof of Funds: GIC vs. 6-Month Bank Statements—Which Is Safer In 2026?

Publish On: December 04, 2025

Proof of Funds is more than a bank balance. For IRCC, it represents economic stability, genuine intent to study in Canada, and the ability to sustain yourself without becoming financially vulnerable in Canada.

To meet POF requirements, a student must demonstrate the ability to cover:

- One year of living expenses

- One year of tuition

- Travel and settlement costs

What Exactly Is a GIC and Why Do Students Prefer It?

A Guaranteed Investment Certificate (GIC) is a financial product offered by Canadian banks such as Scotiabank, RBC, CIBC, BMO, ICICI Canada, and SBI Canada. Under the SDS system, students from eligible countries must purchase a GIC before submitting their study permit application.

What makes GIC unique is its structure:

- The student deposits the funds directly into a Canadian bank.

- The bank issues an official document confirming the deposit.

- Upon arrival in Canada, the student receives a portion of the money upfront for initial expenses.

- The rest is released in monthly installments throughout the first year.

This mechanism benefits both the student and IRCC.

For students, it acts as a financial starter kit in Canada — offering scheduled monthly income.

For IRCC, it is the most dependable form of financial proof because the money is transferred, verified, and fully traceable.

There are no sudden deposits.

- No hidden sources.

- No fluctuations.

- No ambiguity.

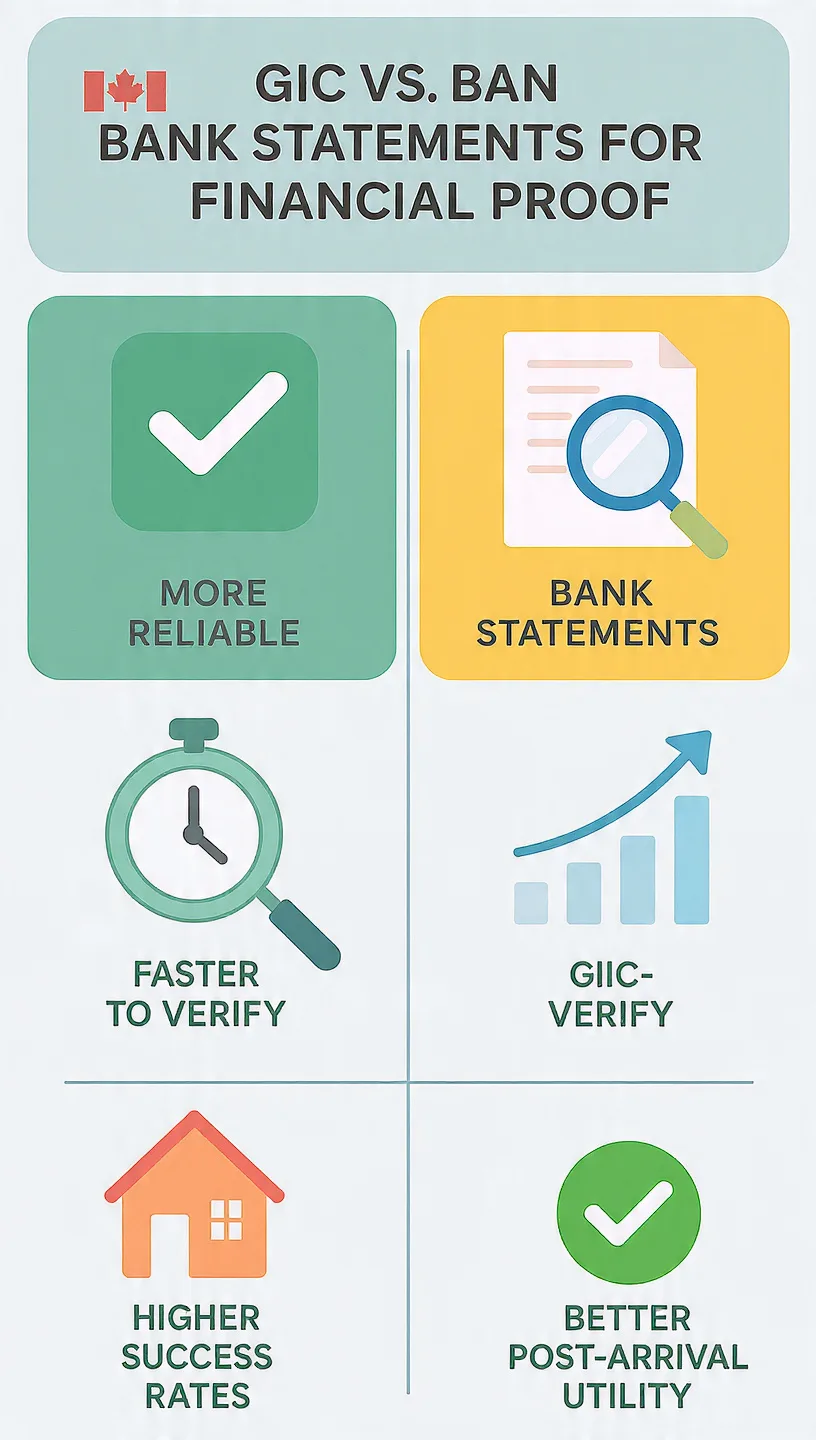

The transparency and simplicity of the GIC is exactly why it is the backbone of SDS applications and why approval rates under SDS are traditionally much higher compared to non-SDS filings.

Understanding 6-Month Bank Statements and How IRCC Evaluates Them

While GICs act as a highly standardized proof, bank statements are far more variable. Every student has a different banking pattern, financial background, and saving habits. When you submit a 6-month bank statement, IRCC examines:

- The consistency of savings

- The stability of the income source

- The presence of unexplained large deposits

- Withdrawal patterns

- Whether the funds are genuinely yours or borrowed temporarily

- How long the money has been in the account

Bank statements not only reflect financial ability but also financial behavior. A fluctuating account or a recent large deposit often raises red flags for visa officers. Even if your total balance is sufficient, IRCC may still refuse the application if the financial pattern appears unstable.

This is why bank statements are more commonly scrutinized and why many students receive refusals with the phrase:

“Your financial resources are not sufficient or credible.”

GICs almost never face this level of scrutiny.

GIC vs. 6-Month Bank Statements:

To truly determine which option is safer, you must understand what IRCC values most: clarity and credibility.

1. Transparency of Funds

A GIC involves a direct international transfer into a Canadian financial institution. The funds are locked in and cannot be manipulated. This creates a clean, verifiable financial trail.

Bank statements, however, may show:

- Irregular deposits

- Mixed funds from multiple sources

- Recent lump-sum credits

- Loans disguised as savings

Even if legitimate, these patterns may create doubts.

Advantage: GIC

2. IRCC Trust Level and Processing Simplicity

Because GICs are standardized, IRCC officers can verify them quickly. Every GIC certificate follows the same structure, includes the same details, and is issued by a recognized institution.

Bank statements vary widely across countries, banks, and formats. Officers must analyze them line-by-line, which increases the possibility of misinterpretation.

Advantage: GIC

3. Approval Rate Differences

Historically, SDS applications — which require a GIC — have significantly higher approval rates than non-SDS applications, even when both applicants meet the minimum requirements.

A major reason is that SDS reduces financial ambiguity.

Bank-statement-based applications often struggle because students cannot convincingly demonstrate stability, especially if the account was “decorated” shortly before applying.

Advantage: GIC

4. Practical Benefits for Students

Upon arriving in Canada, students who used a GIC enjoy:

- An immediate payout to help with settling in

- Monthly disbursements that support budgeting

- Easier integration with a Canadian banking system

Bank statements do not provide any of these practical benefits.

Advantage: GIC

5. Flexibility and Applicability

There is one area where bank statements shine: they work for everyone, including those applying under non-SDS or from countries not eligible for SDS.

GICs alone cannot support tuition payment proof, and they do not replace the need to show additional savings for tuition fees.

So in some scenarios, bank statements are necessary.

But necessary doesn’t mean safer.

Advantage: Depends on the applicant

Who Should Choose GIC?

A GIC is ideal for:

- Every student applying under SDS

- Applicants whose bank statements show inconsistent deposits

- Students who recently received financial support from parents

- Applicants who want the safest, most refusal-proof option

- Anyone whose financial documents may raise unnecessary questions

If your goal is a worry-free application and a high approval probability, GIC is the clear winner.

Who Should Choose Bank Statements?

Bank statements are essential when:

- You are applying under non-SDS

- Your savings are stable and long-term

- Your sponsor has a strong financial background

- You can submit consistent statements showing steady income

- You have already paid part of your tuition and want to show additional funds

When done right, bank statements can be just as solid as a GIC — but they require more careful presentation and supporting documents.

Common Reasons Students Get Refused Due to Bank Statements

Bank-statement-based applications often get rejected for the following reasons:

- Sudden or unexplained deposits

- Funds held for less than 6 months

- Income that does not match the account balance

- Heavy withdrawals shortly before applying

- Multiple small accounts instead of one stable account

- Sponsors without documented income

- Insufficient proof of liquid cash

Final Verdict: Which Is Safer — GIC or Bank Statements?

When it comes to clarity, trust, and approval safety, the GIC is unquestionably the safer and more reliable form of Study Permit Proof of Funds. It eliminates uncertainty, boosts the credibility of your application, and aligns perfectly with IRCC’s expectations.

Bank statements remain important — especially for tuition proof — but they demand stability, consistency, and thorough explanation.

If your goal is to maximize approval chances and avoid financial refusals, use a GIC, supported by clear bank documentation.